US Stocks Rise Despite Hot Inflation

US Inflation Jumps Again

US stocks are pushing higher today despite hotter-than-expected US inflation yesterday and ongoing uncertainty around US/Iran peace talks. Yesterday, US CPI was seen pushing up to 3.8%, hitting its highest level since 2023, stoking rising expectations of a Fed rate hike by year end. The market is currently pricing around a 35% chance of a hike by year end with that projection likely to rise further this week if we see similar strength in PPI and retail sales figures due today and tomorrow respectively. However, it seems that stocks have been unphased by the data with S&P futures pushing higher today ahead of the cash open.

Morgan Stanley Lifts Price Target

Indeed, in a note issued today Morgan Stanley has now upgraded its end of year target for the index to $8000, up from $7800 previously. The bank notes that traders aren’t necessarily ignoring the risks linked to the Iran war but that they have already been priced in, while the developing outlook continues to improve. Though the market’s outlook has shifted away from expecting any more Fed rate cuts this year, the Fed is broadly expected to stay on hold (with rate hike chances still relatively muted). As such, the bank believes conditions are ripe for stocks to continue higher, boosted by good earnings growth. Additionally, should we see a breakthrough in peace talks and a deal materialise, this will pave the way for a much higher push in equities near-term.

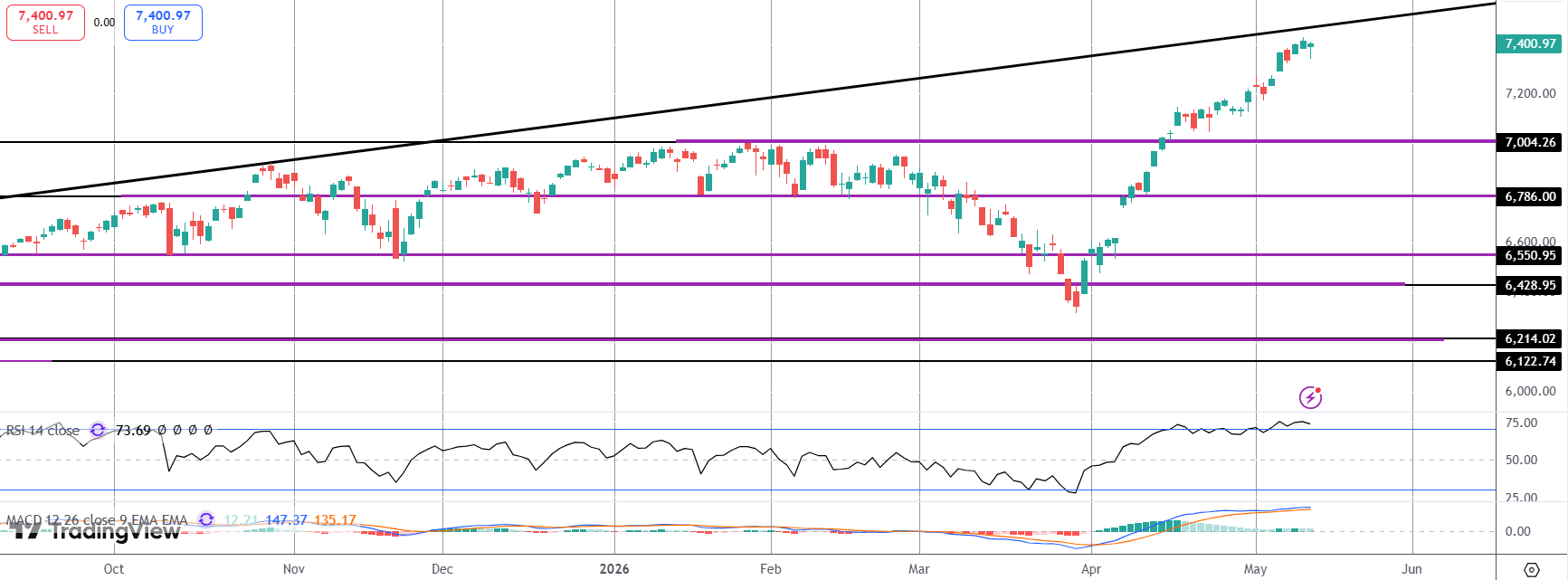

Technical Views

S&P 500

The index remains just under highs, on the back of a solid near-15% run since the March lows. Stalled just ahead of bullish trend line resistance and with momentum studies weakening, risks of a correction lower are see. However, while price holds above the 7k level, focus is on continuation higher with 8k the next bull target.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

With 10 years of experience as a private trader and professional market analyst under his belt, James has carved out an impressive industry reputation. Able to both dissect and explain the key fundamental developments in the market, he communicates their importance and relevance in a succinct and straight forward manner.